A recente retoma económica em Portugal criou duas ilusões de sinal oposto.

Os adeptos do governo da geringonça acreditam que a reversão das medidas de austeridade sem agravamento do défice, explicam a sua inutilidade e a retoma económica.

Os defensores do anterior governo acreditam que a retoma económica não seria possível sem a austeridade que tiveram que aplicar.

Estão ambos enganados.

A austeridade seletiva não eliminou os problemas estruturais que levaram à quase bancarrota do país, de outro modo a reversão das medidas por este governo já teria levado ao agravamento do défice nas contas públicas.

Diz-se que tal só não está a ocorrer porque o governo continua a controlar o défice através de uma austeridade disfarçada (divida a fornecedores, cativações e outros expedientes). Isto é, estaria a escrever direito por linhas tortas, reduzindo o défice à custa do consumo e investimento público, mas restabelecendo os privilégios dos funcionários públicos e o poder do PCP/CGTP/sindicatos nos setores protegidos da concorrência internacional.

Tal poderá ser verdade, mas não explica a retoma económica nem o renascer do otimismo entre os Portugueses. Em relação ao otimismo, para além da tradicional tendência que temos para alternar entre euforia e pessimismos excessivos, tratar-se-á sobretudo do tipo de otimismo daqueles que perdidos no deserto encontram um pequeno oásis que lhes permite sobreviver mais um tempo.

Relembremos alguns dados dos processos de ajustamento vividos em Portugal.

No final do período de três anos do programa da Troika, o ajustamento alcançado na conta corrente de Portugal era semelhante ao dos programas anteriores (8,8% contra 7,7% e 10,1% em 1978 e 1983, respetivamente). No entanto, desta vez, a correção demorou o dobro do tempo e o custo em termos de queda de produção mais do que duplicou (uma queda de 5,2%, contra uma desaceleração de 2,7% em 1978 e uma perda de 2,1% em 1983).

E o que é que aconteceu no período pós-programa? Ao programa de 1978-90 seguiu-se a recessão internacional de 1981-82 pelo que ao fim de três anos tivemos de recorrer a novo programa de ajustamento. O programa seguinte não sofreu a mesma sorte porque entramos para a União Europeia em 1986 e os fundos comunitários vieram adiar por muitos anos os nossos problemas estruturais na balança de pagamentos.

O pós-programa de 2011-2013, também está a beneficiar de três fatores externos positivos muito significativos – o desvio do turismo do norte de África para Portugal e Espanha, a intervenção do Banco Central Europeu e a desvalorização salarial adotada no programa. Porém, nem a magnitude nem a duração estes fatores se podem comparar à entrada na União Europeia.

Por isso, se não mudarmos de rumo, a atual acalmia não durará, na melhor das hipóteses, uma dúzia de anos.

Não vale a pena iludirmo-nos de que estamos a escrever direito por linhas tortas.

Showing posts with label Troika. Show all posts

Showing posts with label Troika. Show all posts

Saturday, 15 July 2017

Wednesday, 4 February 2015

Micro and Macro stories about another Greek bailout

The Greek finance minister European tour of charm has some reasonable ideas in terms of financial engineering. Unfortunately, adjustment is about operational restructuring and only when this has been agreed should the financial engineering solution be designed. I will explain why through two stories.

First the micro story: imagine that Greece is a large corporation running three different businesses. The first business has a good customer basis (e.g. healthcare) but low profits because of over manning. The second has a very long payback period (e.g. infrastructure) and will only turn a profit after a decade. The third is a loss making business (e.g. corporate welfare) with a bleak outlook in terms of future returns. Overall, the company is heavily indebted and runs at a small profit or loss.

Let us consider three restructuring options: a) close down business 3, sell business 2 and use proceeds to refinance business 1; b) refinance existing debt, declare a wage cut for all businesses, stop any further investments in business 2 and reorganize business 3; and c) draw some idealistic reorganization plans and try to convince the creditors that it can only repay them by investing more in the three businesses.

Restructuring plan a) is what a private sector company might do. It would not be the most efficient, because it would not solve the over manning and would jeopardise its service quality and client base. It would continue a lousy business but generating enough cash to keep the creditors happy.

Plan b) is what one may call a restructuring a la Troika. It would ease the financial pressure in the short term but would not improve any of the businesses. Business 3 would still run at a loss and businesses 2 and 1 would deteriorate in both quality and customer base.

Plan c) we may call it a wishful thinking Syriza plan. If “romantic” creditors bought it, they would only throw good money after bad money. The promised growth, even if it happens, will not be enough or sustainable and will only last as long credit keeps flowing in.

Now for the macro story. Of course, if restructuring was done along private sector lines (option 1) the company will not need to worry much about what would happen to businesses 3 and 2, since business 1 was small in relation to the rest of the economy. However, this a fundamental difference in relation to Greece. The country as a whole could not ignore the macro consequences of plan 1, because aggregate demand would reduce significantly causing economic decline instead of growth with a consequent rise in unemployment. So, what could the central bank and budgetary authorities do to minimize such effects?

If they had their own currency (which Greece no longer has), they could devalue it to ensure that real (not nominal) wages would decline making the country as a whole more competitive and hope that the unemployed would quickly get a new job in the export oriented industries. This could be supplemented by printing money, retraining and many other supply side measures. Whether this was enough is not relevant because Greece wants to remain in the Euro and the ECB cannot manage the Euro to meet the needs of Greece. Moreover, Greece is indeed the heavily indebted company and would need extra credit to finance such measures, credit that she no longer may create and has difficulty to obtain in the financial markets.

As expected, see my 2011 post, plan b) has already failed with dramatic declines in GDP and employment. Plan c) could ease the current social disaster in the short run but would make the current imbalances much worse, by compounding over manning across all businesses, perpetuating loss making businesses and government mismanagement.

So, which macro policies can be implemented to emulate a better private sector restructuring plan compatible with economic growth? Basically by providing extra funding and refinancing based on strict conditionality to impose a modified private restructuring plan.

These modifications should involve a mandatory reduction of over manning in the surviving businesses 1 and 2. All redundant workers should be paid a temporary unemployment benefit plus grants to promote labour mobility and the creation of self-employment businesses. The business sector 2 should be capitalized and progressively privatized to maintain a minimum level of investment on a selective basis (only for projects with a short payback period or export orientation). Internal devaluation should be achieved by longer working hours paid in non-negotiable long term government bonds. The fiscal and welfare systems should be entirely revamped and simplified to eradicate tax evasion, free riding and corruption.

As long as conditionality forces the Greeks to use their well-known creativity in the right direction, instead of accounting and fiscal tricks, they will come up with many other ideas and we do not need to enter into further details here.

What Greece, Europe and its creditors cannot afford is to let the Greeks deviate from following a private sector type of restructuring. Without such conditionality, any moratoria, debt swaps, special funds and other types of financial engineering are a waste of money.

Otherwise, everyone risks being caught into a loose-loose dispute between Syriza’s loony left agenda and the Troika’s austerity fairy tale that self-flagellation creates by itself an invigorated economy.

First the micro story: imagine that Greece is a large corporation running three different businesses. The first business has a good customer basis (e.g. healthcare) but low profits because of over manning. The second has a very long payback period (e.g. infrastructure) and will only turn a profit after a decade. The third is a loss making business (e.g. corporate welfare) with a bleak outlook in terms of future returns. Overall, the company is heavily indebted and runs at a small profit or loss.

Let us consider three restructuring options: a) close down business 3, sell business 2 and use proceeds to refinance business 1; b) refinance existing debt, declare a wage cut for all businesses, stop any further investments in business 2 and reorganize business 3; and c) draw some idealistic reorganization plans and try to convince the creditors that it can only repay them by investing more in the three businesses.

Restructuring plan a) is what a private sector company might do. It would not be the most efficient, because it would not solve the over manning and would jeopardise its service quality and client base. It would continue a lousy business but generating enough cash to keep the creditors happy.

Plan b) is what one may call a restructuring a la Troika. It would ease the financial pressure in the short term but would not improve any of the businesses. Business 3 would still run at a loss and businesses 2 and 1 would deteriorate in both quality and customer base.

Plan c) we may call it a wishful thinking Syriza plan. If “romantic” creditors bought it, they would only throw good money after bad money. The promised growth, even if it happens, will not be enough or sustainable and will only last as long credit keeps flowing in.

Now for the macro story. Of course, if restructuring was done along private sector lines (option 1) the company will not need to worry much about what would happen to businesses 3 and 2, since business 1 was small in relation to the rest of the economy. However, this a fundamental difference in relation to Greece. The country as a whole could not ignore the macro consequences of plan 1, because aggregate demand would reduce significantly causing economic decline instead of growth with a consequent rise in unemployment. So, what could the central bank and budgetary authorities do to minimize such effects?

If they had their own currency (which Greece no longer has), they could devalue it to ensure that real (not nominal) wages would decline making the country as a whole more competitive and hope that the unemployed would quickly get a new job in the export oriented industries. This could be supplemented by printing money, retraining and many other supply side measures. Whether this was enough is not relevant because Greece wants to remain in the Euro and the ECB cannot manage the Euro to meet the needs of Greece. Moreover, Greece is indeed the heavily indebted company and would need extra credit to finance such measures, credit that she no longer may create and has difficulty to obtain in the financial markets.

As expected, see my 2011 post, plan b) has already failed with dramatic declines in GDP and employment. Plan c) could ease the current social disaster in the short run but would make the current imbalances much worse, by compounding over manning across all businesses, perpetuating loss making businesses and government mismanagement.

So, which macro policies can be implemented to emulate a better private sector restructuring plan compatible with economic growth? Basically by providing extra funding and refinancing based on strict conditionality to impose a modified private restructuring plan.

These modifications should involve a mandatory reduction of over manning in the surviving businesses 1 and 2. All redundant workers should be paid a temporary unemployment benefit plus grants to promote labour mobility and the creation of self-employment businesses. The business sector 2 should be capitalized and progressively privatized to maintain a minimum level of investment on a selective basis (only for projects with a short payback period or export orientation). Internal devaluation should be achieved by longer working hours paid in non-negotiable long term government bonds. The fiscal and welfare systems should be entirely revamped and simplified to eradicate tax evasion, free riding and corruption.

As long as conditionality forces the Greeks to use their well-known creativity in the right direction, instead of accounting and fiscal tricks, they will come up with many other ideas and we do not need to enter into further details here.

What Greece, Europe and its creditors cannot afford is to let the Greeks deviate from following a private sector type of restructuring. Without such conditionality, any moratoria, debt swaps, special funds and other types of financial engineering are a waste of money.

Otherwise, everyone risks being caught into a loose-loose dispute between Syriza’s loony left agenda and the Troika’s austerity fairy tale that self-flagellation creates by itself an invigorated economy.

Tuesday, 27 January 2015

More on Greece: Krugman’s utopia or folly?

Nobel Laureate Paul Krugman’s case for reducing Greece’s debt service so that she no longer needs to run a large budget surplus is the following: “Suppose that the multiplier is 1.3 — which is what IMF estimates seem to suggest — and that Greece can collect 40 percent of a rise in GDP in revenue (roughly matching its average revenue/GDP). Then an additional billion euros in spending should generate around 0.5 billion euros in revenue, reducing the primary surplus by only 0.5 billion euros”.

However, his back-of-the-envelope calculation is based on an unfounded optimism about the public spending multiplier. I know that he knows that the multiplier effects of spending (public or private) are reduced through import and saving leakages. But, what he (and other optimists) usually miss is that such leakages are extremely dependent on the confidence about the spending policies being implemented.

For instance, if Greek politicians are not credible the multiplier could suddenly reduce to 0.5 and the primary surplus would be reduced by 0.8 billion euros. Or, even worse, if the ruling party is seen as revolutionary, as is the case with Syriza, the leakages may even turn the multiplier into negative values (e.g. -0.5), in which case the primary surplus reduction would be 1.2 billion euros and the current surplus would quickly vanish and destroy any lenders’ willingness to refinance the current debt level ad aeternum.

Indeed, without their own currency, capital controls and the possibility of imposing trade barriers, the leakage through imports is inevitable. Likewise the fear of the radical Syriza policies will accelerate capital flight which is a form of “hoarding”. Moreover, an unexperienced left wing political coalition is usually the most fertile ground for corruption and mismanagement which again act as a form of “hoarding”. In a country already plagued by a culture of corruption, a change towards a “loony left” will only exacerbate the problem.

In conclusion, Krugman’s call to give more importance to debt flows than debt stocks is not a folly, but in Greece’s circumstances it is certainly utopia. So the European countries should only agree to more public spending if Syriza passes a test of political responsibility and can be tied up to a properly designed adjustment program (not the ones implemented in the past by the Troika).

However, his back-of-the-envelope calculation is based on an unfounded optimism about the public spending multiplier. I know that he knows that the multiplier effects of spending (public or private) are reduced through import and saving leakages. But, what he (and other optimists) usually miss is that such leakages are extremely dependent on the confidence about the spending policies being implemented.

For instance, if Greek politicians are not credible the multiplier could suddenly reduce to 0.5 and the primary surplus would be reduced by 0.8 billion euros. Or, even worse, if the ruling party is seen as revolutionary, as is the case with Syriza, the leakages may even turn the multiplier into negative values (e.g. -0.5), in which case the primary surplus reduction would be 1.2 billion euros and the current surplus would quickly vanish and destroy any lenders’ willingness to refinance the current debt level ad aeternum.

Indeed, without their own currency, capital controls and the possibility of imposing trade barriers, the leakage through imports is inevitable. Likewise the fear of the radical Syriza policies will accelerate capital flight which is a form of “hoarding”. Moreover, an unexperienced left wing political coalition is usually the most fertile ground for corruption and mismanagement which again act as a form of “hoarding”. In a country already plagued by a culture of corruption, a change towards a “loony left” will only exacerbate the problem.

In conclusion, Krugman’s call to give more importance to debt flows than debt stocks is not a folly, but in Greece’s circumstances it is certainly utopia. So the European countries should only agree to more public spending if Syriza passes a test of political responsibility and can be tied up to a properly designed adjustment program (not the ones implemented in the past by the Troika).

Monday, 26 January 2015

The lesser evil for Greece and Europe

By electing the Syriza party, the Greeks in despair have turned what was an untenable situation into a nightmare scenario, perhaps hoping to force some kind of way out from the present situation.

What are in fact the Greek options? Using my academic hat I will put them bluntly and leave to others the task of dressing them in politically correct language. The options are basically three.

The first is that once in power, Tsipras and other radical leaders in the coalition will become realists and will not rock the boat. The second is that he will try to implement his political and economic agenda and will end up in mayhem and forced out of the Euro, or, in a worst case scenario, exit the EU and fall back into dictatorship. The third option is that he will declare a moratorium or some other form of debt default and will end up being bailed out again by the Troika.

There are several international experiences we may use as an analogy for each scenario.

The “get real” hypothesis has two versions: a) the FT hope that Tsipras becomes a Lula da Silva rather than a Hugo Chaves; and, b) Krugman’s (socialist) wishful thinking that the sudden abandonment of austerity will revive the Greek economy and the political mess will disappear. Both are very unlikely. The first, because the ideological base of Tsipras is fundamentally different from that of the Lula’s party in Brazil and the financial situation is much worse in Greece. The second ignores that the moderate socialist left has been almost wiped out of the political map and replaced by radicals without previous government experience.

The “mayhem and Euro exit” scenario is the most dangerous for Greece and Europe, if one judges from historical precedents such as the Cuban revolution or the rise of Nazism in Germany. One should not forget that it was economic anarchy, national humiliation, anti-Semitism and the fear of communism that led the Germans to vote Hitler into power. The fact that Syriza has chosen as coalition partner a nationalistic anti-Semite party and left-wing leaders in Southern Europe are increasingly endorsing anti-Semitism under the guise of pro-Palestinian support, creates an environment favorable to the Greek Golden Dawn neo-Nazi party which came third in the election.

The “new debt restructuring and new bailout” is the lesser of the three evils. In practice it means that the Troika needs to develop a new financing mechanism to lend Greece the money they need to repay their debt. This way of preventing a formal write-off of loans from international financial institutions, which enjoy preferred creditor status, has been used by the World Bank through AID lending and by the IMF through the HIPC/MDRI and PRGT Initiatives. Two countries with recently overdue repayments to the IMF were Zimbabwe and Argentina. Both with left-leaning, populist leaders who decided to challenge the international lenders. The results have been years of economic decline and rampant corruption. So, Greece, a country already rigged by alarming levels of corruption, might follow their path. However, for the good of Greece, one should hope that Tsipras will be more like Cristina Kirchner than Robert Mugabe.

To close this rather bleak outlook, I must address the question on whether there are no solutions for the Greek problem. Yes, there are. And I have written about some of them in other posts (e.g. here and here) in 2011, at the start of the Southern European crisis.

However, I do not foresee a possibility that someone will endorse them before the Greek electorates gets disillusioned with the new utopia, votes for more reliable politicians and the EU leaders reconsider their austerity bias. I hope that time will prove me wrong.

What are in fact the Greek options? Using my academic hat I will put them bluntly and leave to others the task of dressing them in politically correct language. The options are basically three.

The first is that once in power, Tsipras and other radical leaders in the coalition will become realists and will not rock the boat. The second is that he will try to implement his political and economic agenda and will end up in mayhem and forced out of the Euro, or, in a worst case scenario, exit the EU and fall back into dictatorship. The third option is that he will declare a moratorium or some other form of debt default and will end up being bailed out again by the Troika.

There are several international experiences we may use as an analogy for each scenario.

The “get real” hypothesis has two versions: a) the FT hope that Tsipras becomes a Lula da Silva rather than a Hugo Chaves; and, b) Krugman’s (socialist) wishful thinking that the sudden abandonment of austerity will revive the Greek economy and the political mess will disappear. Both are very unlikely. The first, because the ideological base of Tsipras is fundamentally different from that of the Lula’s party in Brazil and the financial situation is much worse in Greece. The second ignores that the moderate socialist left has been almost wiped out of the political map and replaced by radicals without previous government experience.

The “mayhem and Euro exit” scenario is the most dangerous for Greece and Europe, if one judges from historical precedents such as the Cuban revolution or the rise of Nazism in Germany. One should not forget that it was economic anarchy, national humiliation, anti-Semitism and the fear of communism that led the Germans to vote Hitler into power. The fact that Syriza has chosen as coalition partner a nationalistic anti-Semite party and left-wing leaders in Southern Europe are increasingly endorsing anti-Semitism under the guise of pro-Palestinian support, creates an environment favorable to the Greek Golden Dawn neo-Nazi party which came third in the election.

The “new debt restructuring and new bailout” is the lesser of the three evils. In practice it means that the Troika needs to develop a new financing mechanism to lend Greece the money they need to repay their debt. This way of preventing a formal write-off of loans from international financial institutions, which enjoy preferred creditor status, has been used by the World Bank through AID lending and by the IMF through the HIPC/MDRI and PRGT Initiatives. Two countries with recently overdue repayments to the IMF were Zimbabwe and Argentina. Both with left-leaning, populist leaders who decided to challenge the international lenders. The results have been years of economic decline and rampant corruption. So, Greece, a country already rigged by alarming levels of corruption, might follow their path. However, for the good of Greece, one should hope that Tsipras will be more like Cristina Kirchner than Robert Mugabe.

To close this rather bleak outlook, I must address the question on whether there are no solutions for the Greek problem. Yes, there are. And I have written about some of them in other posts (e.g. here and here) in 2011, at the start of the Southern European crisis.

However, I do not foresee a possibility that someone will endorse them before the Greek electorates gets disillusioned with the new utopia, votes for more reliable politicians and the EU leaders reconsider their austerity bias. I hope that time will prove me wrong.

Wednesday, 30 April 2014

Condecorações Inoportunas

O Presidente da República condecora hoje António Mexia presidente da EDP. De momento não me ocorre nenhum serviço público relevante prestado pelo condecorado, mas seguramente que a Presidência invocará alguns. No entanto, o momento parece-me infeliz.

Numa altura em que a Troika procura fazer cumprir a sua promessa tímida de reduzir as rendas excessivas no sector das energias, condecorar o principal lider da oposição a essa redução é no mínimo incompreensível.

Mas não só. Acontece também que no imaginário popular esse gestor é dos mais bem pagos no país e aparece aos olhos do povo como o símbolo da ganância e indiferença perante os sacrifícios impostos à generalidade dos Portugueses.

Têm duvidas? Vejamos os fatos comparando os biénios pré e pós Troika.

Entre 2010 e 2012 a evolução dos preços da energia em Portugal comparada à dos outros preços ao consumidor e à do preço do petróleo foi a que podemos observar no seguinte gráfico.

Como podemos constatar, em Junho de 2013 os preços do Petróleo tinham caído 10% mas os preços da energia pagos pelo consumidor Português tinham aumentado 10%, enquanto os preços dos restantes bens permaneceram quase na mesma nos primeiros dois anos pós Troika.

Como podemos constatar, em Junho de 2013 os preços do Petróleo tinham caído 10% mas os preços da energia pagos pelo consumidor Português tinham aumentado 10%, enquanto os preços dos restantes bens permaneceram quase na mesma nos primeiros dois anos pós Troika.

Entretanto, o que aconteceu às remunerações desse quando comparadas com, por exemplo, um professor universitário. O último recebeu ilíquidos no biénio pré Troika 119.1 mil Euros e no pós Troika 99.6 mil Euros, tendo sofrido um corte salarial de 16.4%. Nos mesmos biénios António Mexia recebeu, respetivamente, 2358 e 2257 milhares de Euros pelo que teve um corte de apenas 5.1%.

Será que tamanha diferença se explica pelo desempenho das empresas dirigidas por esse gestor? Os números mostram que não. Nos mesmos biénios os resultados por ação da EDP subiram apenas de 58 para 59 cêntimos.

Que a Presidência da República tenha ignorado estes factos é no mínimo incompreensível

Porém, as consequências são graves a três níveis:

a) Transmite uma imagem de subordinação do poder político ao poder económico, dando à Troika um pretexto para esquecer mais uma vez o objetivo de redução das rendas excessivas no setor energético;

b) Agrava o sentimento de injustiça que o povo sente na distribuição dos sacrifícios impostos pelo programa de ajustamento; e, sobretudo

c) Desprestigia a Presidência da República enquanto último garante dos Portugueses, aparecendo cada vez mais alheada do povo e da realidade.

Pessoalmente, tendo integrado da Comissão de Apoio à reeleição do Presidente da República, entristece-me vê-lo aproximar-se do final do seu mandato numa posição que me faz lembrar a de Américo Tomás no regime anterior ao 25 de Abril.

As condecorações, tal como outros gestos simbólicos, valem pela oportunidade com que são atribuídos. Por isso, não podemos deixar de considerar esta condecoração como tão inoportuna que até parece uma afronta aos Portugueses.

P.S. Numa versão anterior deste post tinhamos incluido o nome de Ferreira de Oliveira, Presidente da Galp, que na notícia que ouvimos na rádio confundimos com o de Faria de Oliveira. As nossas desculpas ao visado por este equivoco.

Numa altura em que a Troika procura fazer cumprir a sua promessa tímida de reduzir as rendas excessivas no sector das energias, condecorar o principal lider da oposição a essa redução é no mínimo incompreensível.

Mas não só. Acontece também que no imaginário popular esse gestor é dos mais bem pagos no país e aparece aos olhos do povo como o símbolo da ganância e indiferença perante os sacrifícios impostos à generalidade dos Portugueses.

Têm duvidas? Vejamos os fatos comparando os biénios pré e pós Troika.

Entre 2010 e 2012 a evolução dos preços da energia em Portugal comparada à dos outros preços ao consumidor e à do preço do petróleo foi a que podemos observar no seguinte gráfico.

Entretanto, o que aconteceu às remunerações desse quando comparadas com, por exemplo, um professor universitário. O último recebeu ilíquidos no biénio pré Troika 119.1 mil Euros e no pós Troika 99.6 mil Euros, tendo sofrido um corte salarial de 16.4%. Nos mesmos biénios António Mexia recebeu, respetivamente, 2358 e 2257 milhares de Euros pelo que teve um corte de apenas 5.1%.

Será que tamanha diferença se explica pelo desempenho das empresas dirigidas por esse gestor? Os números mostram que não. Nos mesmos biénios os resultados por ação da EDP subiram apenas de 58 para 59 cêntimos.

Que a Presidência da República tenha ignorado estes factos é no mínimo incompreensível

Porém, as consequências são graves a três níveis:

a) Transmite uma imagem de subordinação do poder político ao poder económico, dando à Troika um pretexto para esquecer mais uma vez o objetivo de redução das rendas excessivas no setor energético;

b) Agrava o sentimento de injustiça que o povo sente na distribuição dos sacrifícios impostos pelo programa de ajustamento; e, sobretudo

c) Desprestigia a Presidência da República enquanto último garante dos Portugueses, aparecendo cada vez mais alheada do povo e da realidade.

Pessoalmente, tendo integrado da Comissão de Apoio à reeleição do Presidente da República, entristece-me vê-lo aproximar-se do final do seu mandato numa posição que me faz lembrar a de Américo Tomás no regime anterior ao 25 de Abril.

As condecorações, tal como outros gestos simbólicos, valem pela oportunidade com que são atribuídos. Por isso, não podemos deixar de considerar esta condecoração como tão inoportuna que até parece uma afronta aos Portugueses.

P.S. Numa versão anterior deste post tinhamos incluido o nome de Ferreira de Oliveira, Presidente da Galp, que na notícia que ouvimos na rádio confundimos com o de Faria de Oliveira. As nossas desculpas ao visado por este equivoco.

Wednesday, 12 February 2014

Programa Cautelar: Sim ou não?

A opinião pública Portuguesa está dividida entre os mais cautelosos, que defendem que Portugal devia recorrer a um programa cautelar, e os arrojados que advogam a chamada saída limpa do programa de ajustamento para retomar a onda despesista e/ou camuflar o falhanço do programa da Troika.

Infelizmente, os mais prudentes não têm razão. Em teoria um programa cautelar é uma boa ideia, mas na realidade tais programas podem trazer mais desconfianças do que certezas.

A política de programas cautelares foi introduzida pelo FMI na sequência da crise Asiática de 1998, através das chamadas Contingent Credit Lines, mas em 2003 ninguém ainda tinha recorrido a essa medida que entretanto foi abandonada. A principal razão para a sua não utilização foi atribuída pelo FMI ao facto dos países elegíveis temerem que o recurso a essa medida fosse interpretado pelos mercados como um sinal de fraqueza e não de solidez.

Tal receio é fundado, como podemos ilustrar através de uma analogia simples. A Troika, tal como qualquer professor, tem vantagem em subavaliar o mau desempenho dos seus devedores (alunos) de forma a convencer os mercados (empregadores) a financiar (empregar) os participantes no seu programa.

Por exemplo, se este ano tivesse utilizado a minha exigência habitual mais de 60% dos meus alunos teria chumbado e no próximo ano o meu trabalho quase duplicaria. Em alternativa, podia passá-los de forma limpa, isto é subindo as notas entre 7 e 9 para dez sem quaisquer condições, ou dar-lhes 10 valores condicionados à frequência de aulas suplementares. Esta solução parece a mais razoável, mas na verdade era pior para mim (mais aulas) e para eles (menos oportunidades de emprego) porque os empregadores iriam interpretar a frequência de aulas suplementares como sinal de fraqueza e preteri-los no seu recrutamento.

Em conclusão, embora a “passagem administrativa” de Portugal no seu programa de ajustamento não augure um futuro brilhante para o nosso país, é preferível deixá-lo livre para tentar encontrar uma saída da crise ou voltar a pedir um novo programa de ajustamento dentro de três a cinco anos. Infelizmente, o programa de investimentos públicos já anunciado para o próximo QREN é mais uma lista de “elefantes brancos” sem qualquer rentabilidade, que agravará as disparidades regionais e faz antever que não evitaremos mais programas de ajustamento no futuro.

Infelizmente, os mais prudentes não têm razão. Em teoria um programa cautelar é uma boa ideia, mas na realidade tais programas podem trazer mais desconfianças do que certezas.

A política de programas cautelares foi introduzida pelo FMI na sequência da crise Asiática de 1998, através das chamadas Contingent Credit Lines, mas em 2003 ninguém ainda tinha recorrido a essa medida que entretanto foi abandonada. A principal razão para a sua não utilização foi atribuída pelo FMI ao facto dos países elegíveis temerem que o recurso a essa medida fosse interpretado pelos mercados como um sinal de fraqueza e não de solidez.

Tal receio é fundado, como podemos ilustrar através de uma analogia simples. A Troika, tal como qualquer professor, tem vantagem em subavaliar o mau desempenho dos seus devedores (alunos) de forma a convencer os mercados (empregadores) a financiar (empregar) os participantes no seu programa.

Por exemplo, se este ano tivesse utilizado a minha exigência habitual mais de 60% dos meus alunos teria chumbado e no próximo ano o meu trabalho quase duplicaria. Em alternativa, podia passá-los de forma limpa, isto é subindo as notas entre 7 e 9 para dez sem quaisquer condições, ou dar-lhes 10 valores condicionados à frequência de aulas suplementares. Esta solução parece a mais razoável, mas na verdade era pior para mim (mais aulas) e para eles (menos oportunidades de emprego) porque os empregadores iriam interpretar a frequência de aulas suplementares como sinal de fraqueza e preteri-los no seu recrutamento.

Em conclusão, embora a “passagem administrativa” de Portugal no seu programa de ajustamento não augure um futuro brilhante para o nosso país, é preferível deixá-lo livre para tentar encontrar uma saída da crise ou voltar a pedir um novo programa de ajustamento dentro de três a cinco anos. Infelizmente, o programa de investimentos públicos já anunciado para o próximo QREN é mais uma lista de “elefantes brancos” sem qualquer rentabilidade, que agravará as disparidades regionais e faz antever que não evitaremos mais programas de ajustamento no futuro.

Wednesday, 17 April 2013

O Impasse Português

Já aqui explicamos por várias vezes as razões pelas quais o programa de ajustamento para Portugal falharia, tal como falhou. No entanto, a visita intercalar da Troika e o falhanço da tentativa atabalhoada do Governo para associar o Partido Socialista às adaptações do programa em curso levam-me a voltar ao tema para explicar o drama da situação Portuguesa.

O drama resulta de termos dois intervenientes igualmente errados sobre o que propõem para Portugal. De um lado temos o Governo/Troika apostados em fazer uma consolidação orçamental a qualquer custo e do outro uma oposição a não querer austeridade em nenhuma circunstância. Em termos simples direi que uns querem mais tempo, mais dinheiro e mais facilidades e os outros acreditam que a “fada mágica” do crescimento nascerá de uma pátria anoréxica em vias de desfalecimento. Nem uns nem outros percebem que não é assim que se recupera uma empresa ou um país.

Em linguagem técnica, os economistas do Governo/Troika continuam a ignorar os efeitos nefastos sobre a procura agregada nacional e o emprego do corte dos rendimentos nominais, denunciados por Keynes nos anos de 1930, e vêm propor menos despesa pública e mais cortes de rendimento para os funcionários públicos e pensionistas. Não percebem a diferença entre o efeito multiplicador do despedimento selectivo dos funcionários públicos em organismos e funções marginais do Estado e uma baixa generalizada da remuneração dos funcionários públicos.

Os Socialistas tentam ressuscitar a ideia Keynesiana de que em situações de desemprego extremo seria mesmo aceitável pagar a uns para abrir buracos e a outros para os tapar. De facto, acabo de ouvir a conferência de imprensa dada por António José Seguro após reunir com Passos Coelho e a Troika e quando questionado sobre políticas concretas de crescimento as duas únicas que citou foram a reabilitação urbana e o investimento em eficiência energética. Na verdade são ambas medidas do tipo abrir e tapar buracos para agradar aos lobbies da construção e das energias renováveis que estiveram na origem da actual crise, porque se esses investimentos forem realmente rentáveis os seus donos encontrarão forma de os financiar. A sugestão Keynesiana do abrir e tapar buracos só foi feita para períodos muito curtos e em circunstâncias onde houvesse margem para agravar o endividamento externo e os défices orçamentais; que não existem em Portugal.

Para facilitar a compreensão das consequências da ignorância do Governo/Troika e da oposição Socialista, o leitor imagine que o Governo em vez de gastar 5 dos 87 mil milhões pedidos à Troika num novo Fundo/Banco e os 12 mil milhões de Euros ainda disponíveis no QREN até 2015 em projectos de utilidade duvidosa decidia gastar 15 mil milhões desse montante para financiar o despedimento de 20% (cerca de 120 mil) funcionários públicos. Essa verba daria para lhes pagar um subsídio de desemprego equivalente a 90% do seu vencimento durante dois anos e ainda dar um subsídio de 50 mil euros a cada para criarem o seu próprio emprego ou empresa. O efeito sobre a sustentabilidade das contas públicas seria permanente e algum desse dinheiro seria mesmo recuperado através dos impostos pagos pelas empresas criadas por esses funcionários.

Em resumo, a compatibilização da consolidação financeira com o crescimento só é possível se houver coragem para combater a ignorância e tibieza do Governo/Troika e da Oposição em Portugal.

O drama resulta de termos dois intervenientes igualmente errados sobre o que propõem para Portugal. De um lado temos o Governo/Troika apostados em fazer uma consolidação orçamental a qualquer custo e do outro uma oposição a não querer austeridade em nenhuma circunstância. Em termos simples direi que uns querem mais tempo, mais dinheiro e mais facilidades e os outros acreditam que a “fada mágica” do crescimento nascerá de uma pátria anoréxica em vias de desfalecimento. Nem uns nem outros percebem que não é assim que se recupera uma empresa ou um país.

Em linguagem técnica, os economistas do Governo/Troika continuam a ignorar os efeitos nefastos sobre a procura agregada nacional e o emprego do corte dos rendimentos nominais, denunciados por Keynes nos anos de 1930, e vêm propor menos despesa pública e mais cortes de rendimento para os funcionários públicos e pensionistas. Não percebem a diferença entre o efeito multiplicador do despedimento selectivo dos funcionários públicos em organismos e funções marginais do Estado e uma baixa generalizada da remuneração dos funcionários públicos.

Os Socialistas tentam ressuscitar a ideia Keynesiana de que em situações de desemprego extremo seria mesmo aceitável pagar a uns para abrir buracos e a outros para os tapar. De facto, acabo de ouvir a conferência de imprensa dada por António José Seguro após reunir com Passos Coelho e a Troika e quando questionado sobre políticas concretas de crescimento as duas únicas que citou foram a reabilitação urbana e o investimento em eficiência energética. Na verdade são ambas medidas do tipo abrir e tapar buracos para agradar aos lobbies da construção e das energias renováveis que estiveram na origem da actual crise, porque se esses investimentos forem realmente rentáveis os seus donos encontrarão forma de os financiar. A sugestão Keynesiana do abrir e tapar buracos só foi feita para períodos muito curtos e em circunstâncias onde houvesse margem para agravar o endividamento externo e os défices orçamentais; que não existem em Portugal.

Para facilitar a compreensão das consequências da ignorância do Governo/Troika e da oposição Socialista, o leitor imagine que o Governo em vez de gastar 5 dos 87 mil milhões pedidos à Troika num novo Fundo/Banco e os 12 mil milhões de Euros ainda disponíveis no QREN até 2015 em projectos de utilidade duvidosa decidia gastar 15 mil milhões desse montante para financiar o despedimento de 20% (cerca de 120 mil) funcionários públicos. Essa verba daria para lhes pagar um subsídio de desemprego equivalente a 90% do seu vencimento durante dois anos e ainda dar um subsídio de 50 mil euros a cada para criarem o seu próprio emprego ou empresa. O efeito sobre a sustentabilidade das contas públicas seria permanente e algum desse dinheiro seria mesmo recuperado através dos impostos pagos pelas empresas criadas por esses funcionários.

Em resumo, a compatibilização da consolidação financeira com o crescimento só é possível se houver coragem para combater a ignorância e tibieza do Governo/Troika e da Oposição em Portugal.

Saturday, 3 November 2012

Why the IMF therapy is not working in Portugal

The IMF repeats in Portugal the ostrich policy of not recognizing what is fundamentally wrong with its adjustment approach in the Euro Area. In its 5th review of the Portuguese program it states that “authorities have made good progress in reducing macroeconomic imbalances … But after a strong start, the program has entered a more challenging phase … a large and durable fiscal gap has emerged due to a shift in the composition of output from domestic demand to less-taxed net-exports”.

Despite the initial Portuguese external disequilibrium being milder than the Greek or Irish, I anticipated that the program was likely to fail because it had been undertaken reluctantly, too late, with too little and it was too soft. Moreover, its management was weak, incompetent and erratic partly because the Troika was desperate to have a success story and it had in Portugal a Finance Minister – Victor Gaspar – that was seen as one of their men. So, all tough measures (e.g. reducing the number of municipalities and monopolistic rents) were abandoned or reversed. For instance, fiscal consolidation which was to be implemented by 2/3 of expenditure cuts and 1/3 of revenue measures failed completely with the expenditure hardly slowing down and the revenue collapsing.

By now the IMF had to agree to extend its program for one more year and to grant some waivers, while it is already busy working on another package that will inevitably result on more time and more money. This will only raise the Portuguese external debt to new heights without any visible improvement in its economic growth.

Just as a reminder, note that the Greek debt path under IMF management, which started in May 2010 with a general government debt equivalent to 115% of GDP and was supposed to peak in 2012 at 149%, at the start of the second IMF bailout in June 2012 had already reached 165% and is expected to peak at 171% in 2014. For comparison, in Greece the total net external debt rose from 87 to 107% of GDP between 2009 and 2012 while in Portugal (external debt, excluding FDI and reserves) rose only from 98 to 99% of GDP. However, the portion owed by the government increased from 64 to 95% of GDP, degenerating into a sovereign debt crisis.

In a recent post we called the current IMF (Troika) adjustment program for Portugal a pyrrhic victory because, when compared to previous programs, it had doubled the cost of external adjustment in terms of output loss. We identified as the main culprit a weak foreign trade multiplier. So, the key question is why isn´t the trade multiplier working now as it did in past programs? As we calculated the multiplier effect by assuming a constant income elasticity of demand for imports the explanation must be accounted for by a sluggish international economic growth and or changes in relative prices (terms of trade).

In fact, the growth of the world economy accounts for a small portion of the reduced multiplier effect, since the OECD was growing at 6% during the first two programs but recently it has been growing at only 4.3%. So, the majority (71%) of the blame for the smaller multiplier effect lies in a weak export performance because of lower price elasticities and adverse changes in the terms of trade. Since recent estimates show that the export price elasticity remains low (0.42) and statistically is not significantly different from zero, the core explanation must lie in the terms of trade.

The Portuguese terms of trade did not deteriorate enough to drive a higher level of economic activity because of an irresponsible fiscal policy of indirect tax increases that caused a futile destruction of businesses in the non-tradable goods sector and the failure to confront the powerful lobbies in the energy and transport sectors that hamper the tradable goods sector. This trend in the terms of trade is clearly visible in the following chart.

The persistence of domestic inflationary forces despite an increase of 3.5 percentage points in the unemployment rate which reached 15.5% can only be the result of market rigidities compounded by fiscal mistakes.

The program of fiscal consolidation was not only inefficient, but foolish and poorly sequenced. Instead of targeting the preservation or a small rise in revenue, through the broadening of the tax base and selective competitive tax cuts, combined with substantial cuts in subsidies and other wasteful forms of spending it did the reverse. In terms of sequencing, instead of beginning with spending cuts, followed by a broadening of the income tax base and cuts in corporate taxes it did the reverse. It raised indirect taxes first at the expense of external competitiveness and is now promising a massive increase in income and corporate taxes for 2013 to be followed by spending cuts in 2014, thus perpetuating unnecessarily the current recession for at least another two years.

In conclusion, the program left untouched all the cancers blocking the growth of the Portuguese economy listed in this blog long ago as being: irresponsible recourse to PPP financing, large rent-seeking privatized monopolies, extensive subsidization of energy, environment, technological and other self-serving mafias, too many, too inefficient and too indebted State enterprises for the exclusive benefit of their managers, unions and bankers, a financial sector who suckles on public financing, the uncontrollable spending of the health and social security sectors, the destruction of a professionally independent public service, dysfunctional fiscal and judicial systems and generalized recourse to off-budget operations and creative accounting. Indeed, it made things worse through mismanagement. So, without changing course, Portugal is condemned to more than a decade of slow growth and unbearable indebtedness and sooner or later it will have to default or ask for debt forgiveness for the first time since 1892.

As a Portuguese I am saddened to see my beloved country ravaged by an incompetent government in collusion with useless international organizations at the mercy of an unholy alliance of heartless Teutonic European mandarins, predatory Chinese and Angolan dictators and dubious Latin American business interests. This is the end result of 80 years of state capitalism in Portugal.

Despite the initial Portuguese external disequilibrium being milder than the Greek or Irish, I anticipated that the program was likely to fail because it had been undertaken reluctantly, too late, with too little and it was too soft. Moreover, its management was weak, incompetent and erratic partly because the Troika was desperate to have a success story and it had in Portugal a Finance Minister – Victor Gaspar – that was seen as one of their men. So, all tough measures (e.g. reducing the number of municipalities and monopolistic rents) were abandoned or reversed. For instance, fiscal consolidation which was to be implemented by 2/3 of expenditure cuts and 1/3 of revenue measures failed completely with the expenditure hardly slowing down and the revenue collapsing.

By now the IMF had to agree to extend its program for one more year and to grant some waivers, while it is already busy working on another package that will inevitably result on more time and more money. This will only raise the Portuguese external debt to new heights without any visible improvement in its economic growth.

Just as a reminder, note that the Greek debt path under IMF management, which started in May 2010 with a general government debt equivalent to 115% of GDP and was supposed to peak in 2012 at 149%, at the start of the second IMF bailout in June 2012 had already reached 165% and is expected to peak at 171% in 2014. For comparison, in Greece the total net external debt rose from 87 to 107% of GDP between 2009 and 2012 while in Portugal (external debt, excluding FDI and reserves) rose only from 98 to 99% of GDP. However, the portion owed by the government increased from 64 to 95% of GDP, degenerating into a sovereign debt crisis.

In a recent post we called the current IMF (Troika) adjustment program for Portugal a pyrrhic victory because, when compared to previous programs, it had doubled the cost of external adjustment in terms of output loss. We identified as the main culprit a weak foreign trade multiplier. So, the key question is why isn´t the trade multiplier working now as it did in past programs? As we calculated the multiplier effect by assuming a constant income elasticity of demand for imports the explanation must be accounted for by a sluggish international economic growth and or changes in relative prices (terms of trade).

In fact, the growth of the world economy accounts for a small portion of the reduced multiplier effect, since the OECD was growing at 6% during the first two programs but recently it has been growing at only 4.3%. So, the majority (71%) of the blame for the smaller multiplier effect lies in a weak export performance because of lower price elasticities and adverse changes in the terms of trade. Since recent estimates show that the export price elasticity remains low (0.42) and statistically is not significantly different from zero, the core explanation must lie in the terms of trade.

The Portuguese terms of trade did not deteriorate enough to drive a higher level of economic activity because of an irresponsible fiscal policy of indirect tax increases that caused a futile destruction of businesses in the non-tradable goods sector and the failure to confront the powerful lobbies in the energy and transport sectors that hamper the tradable goods sector. This trend in the terms of trade is clearly visible in the following chart.

The persistence of domestic inflationary forces despite an increase of 3.5 percentage points in the unemployment rate which reached 15.5% can only be the result of market rigidities compounded by fiscal mistakes.

The program of fiscal consolidation was not only inefficient, but foolish and poorly sequenced. Instead of targeting the preservation or a small rise in revenue, through the broadening of the tax base and selective competitive tax cuts, combined with substantial cuts in subsidies and other wasteful forms of spending it did the reverse. In terms of sequencing, instead of beginning with spending cuts, followed by a broadening of the income tax base and cuts in corporate taxes it did the reverse. It raised indirect taxes first at the expense of external competitiveness and is now promising a massive increase in income and corporate taxes for 2013 to be followed by spending cuts in 2014, thus perpetuating unnecessarily the current recession for at least another two years.

In conclusion, the program left untouched all the cancers blocking the growth of the Portuguese economy listed in this blog long ago as being: irresponsible recourse to PPP financing, large rent-seeking privatized monopolies, extensive subsidization of energy, environment, technological and other self-serving mafias, too many, too inefficient and too indebted State enterprises for the exclusive benefit of their managers, unions and bankers, a financial sector who suckles on public financing, the uncontrollable spending of the health and social security sectors, the destruction of a professionally independent public service, dysfunctional fiscal and judicial systems and generalized recourse to off-budget operations and creative accounting. Indeed, it made things worse through mismanagement. So, without changing course, Portugal is condemned to more than a decade of slow growth and unbearable indebtedness and sooner or later it will have to default or ask for debt forgiveness for the first time since 1892.

As a Portuguese I am saddened to see my beloved country ravaged by an incompetent government in collusion with useless international organizations at the mercy of an unholy alliance of heartless Teutonic European mandarins, predatory Chinese and Angolan dictators and dubious Latin American business interests. This is the end result of 80 years of state capitalism in Portugal.

Tuesday, 30 October 2012

Portugal´s External Adjustment: a Pyrrhic victory

(Post initially published on 30/10/2012. Since the program is now finished we updated in May 2015 the last table with the impact on economic growth and its analysis. The rest of the text and our conclusion remain the same.)

A pyrrhic war is a war won at too high a cost. As Pyrrhus said, in 280 BC: "If we are victorious in one more battle with the Romans, we shall be utterly ruined". Recently, Ireland, Spain and Portugal achieved sharp reductions in their current account deficits as depicted in the table below.

Let us examine if these results are similar to a pyrrhic victory.

Let us examine if these results are similar to a pyrrhic victory.

Indeed, the costs in terms of lost production and related increase in unemployment shown in the table below were so high for Greece and Portugal that one must ask whether for these countries the victors have weakened their economies to a point where they were trapped into a permanent state of lower income and productivity.

There are five basic reasons to fear that it might be the case. First, the adjustment was achieved almost exclusively through output and capacity reduction. Second, the massive conversion of private debt into public debt increased the cost of leverage for all and for a long time which crowded out the most dynamic sector of the economy – the SMEs. Third, the recurrent need for never ending tax increases created a persistent trend for appreciation in their foreign terms of trade, when they needed the opposite. Fourth, it created a permanent stimulus for capital flight. And, finally the resulting increase in long term unemployment raised the level of structural unemployment to unbearable levels.

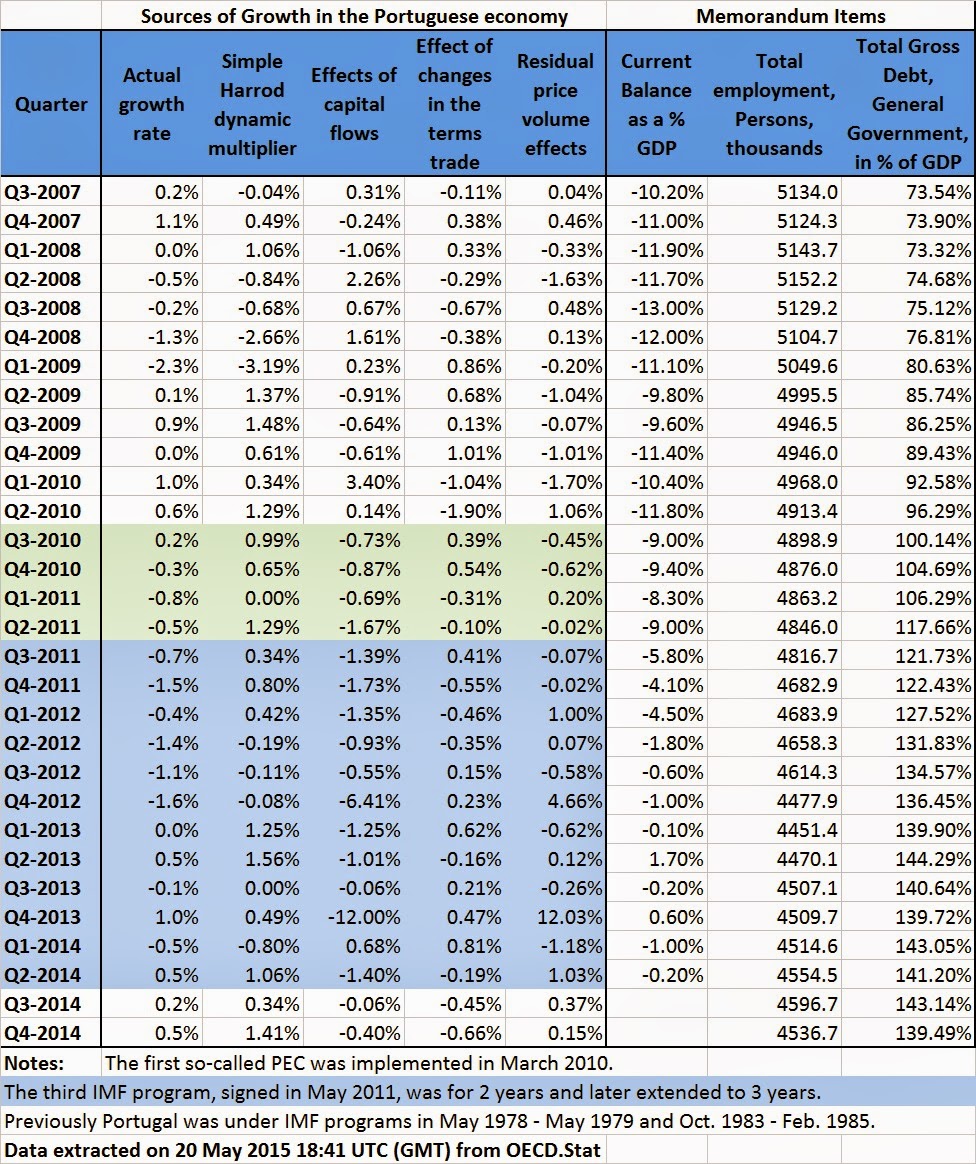

The case of Portugal is especially illustrative because it has duly taken its medicine and achieved the sharpest external correction. We will examine causes one and three above by comparing the current adjustment to that of previous IMF programs in the 1970s and 1980s. The exercise can be done using the financial accounts or through Thirlwall´s balance payments constrained growth accounting framework. I use the later approach to compare the current situation with a similar study I did 20 years ago and which is summarized in the following table with a breakdown of the sources of GDP growth.

The success of the two previous programs can be judged by the reduction in the current account deficit over the first two years and the corresponding cost in terms of output decline. In the first program a reduction of 7.7 percentage points in the current account deficit triggered a slowdown in economic growth only in the first year. The second program achieved a deficit reduction of 10.1 percentage points at a cost of a two-year recession that reduced GDP by 2.1%.

In both programs we measured the role played by the foreign trade multiplier to offset the decline in growth caused by the reduction in capital inflows. In the first program a fall in output due to capital flows of 11.2% was more than offset by a multiplier effect of 19.2%. In the second program a loss of 21.2% caused by a reversal of capital inflows was offset only partially by a 14.5% multiplier effect, but overall in the third year the economy had recovered from the output losses incurred during the 1983-84 recession.

Let us now compare this performance with the current adjustment program for Portugal, as shown in the table below with quarterly values.

During the first year, the pre-Troika PEC adjustment program achieved a reduction in the current account deficit of only 2.8% at a cost of 1.4% in output. The capital effect was responsible for a decline of 3.9% in growth, but was almost offset by a trade multiplier effect of 3.0%.

For the duration of the 3-year IMF adjustment program, the current account deficit was reduced by 8.8 percentage points at a cost of 8.1% in output caused by the program’s effect on capital flows and residual price-volume effects. However, its foreign trade multiplier offset was just 4.8%, which explains why the economic recession has deepened to 5.2% (including the negative impact of terms of a terms of trade improvement brought about an appreciating Euro).

At the end of the program’s three-year period, the adjustment achieved in the current account was similar to that of the previous programs (8.8% against 7.7% and 10.1% in 1978 and 1983, respectively). Yet, this time it took twice as long and the cost in terms of output more than doubled (a 5.2% fall now, against a slowdown of 2.7% in 1978 and a loss of 2.1% in 1983).

In summary:

1) The program achieved its objectives (the current account adjustment and a return to private debt markets); but:

2) It required twice the duration and the output losses of past programs;

3) The banking sector restructuring and fiscal consolidation were negligible. Public debt increased 23.5 percentage points to reach 141.2% of GDP at the end of the program;

4) The social burden was significant, with the unemployment rate rising two percentage points to 14.4%; and

5) There was a minor (0.8%) improvement in productivity because the decline in output was close to the loss of jobs (6%).

For these reasons the Portuguese adjustment must be classified as a pyrrhic victory, which, if repeated, will ruin the country.

A pyrrhic war is a war won at too high a cost. As Pyrrhus said, in 280 BC: "If we are victorious in one more battle with the Romans, we shall be utterly ruined". Recently, Ireland, Spain and Portugal achieved sharp reductions in their current account deficits as depicted in the table below.

Indeed, the costs in terms of lost production and related increase in unemployment shown in the table below were so high for Greece and Portugal that one must ask whether for these countries the victors have weakened their economies to a point where they were trapped into a permanent state of lower income and productivity.

There are five basic reasons to fear that it might be the case. First, the adjustment was achieved almost exclusively through output and capacity reduction. Second, the massive conversion of private debt into public debt increased the cost of leverage for all and for a long time which crowded out the most dynamic sector of the economy – the SMEs. Third, the recurrent need for never ending tax increases created a persistent trend for appreciation in their foreign terms of trade, when they needed the opposite. Fourth, it created a permanent stimulus for capital flight. And, finally the resulting increase in long term unemployment raised the level of structural unemployment to unbearable levels.

The case of Portugal is especially illustrative because it has duly taken its medicine and achieved the sharpest external correction. We will examine causes one and three above by comparing the current adjustment to that of previous IMF programs in the 1970s and 1980s. The exercise can be done using the financial accounts or through Thirlwall´s balance payments constrained growth accounting framework. I use the later approach to compare the current situation with a similar study I did 20 years ago and which is summarized in the following table with a breakdown of the sources of GDP growth.

The success of the two previous programs can be judged by the reduction in the current account deficit over the first two years and the corresponding cost in terms of output decline. In the first program a reduction of 7.7 percentage points in the current account deficit triggered a slowdown in economic growth only in the first year. The second program achieved a deficit reduction of 10.1 percentage points at a cost of a two-year recession that reduced GDP by 2.1%.

In both programs we measured the role played by the foreign trade multiplier to offset the decline in growth caused by the reduction in capital inflows. In the first program a fall in output due to capital flows of 11.2% was more than offset by a multiplier effect of 19.2%. In the second program a loss of 21.2% caused by a reversal of capital inflows was offset only partially by a 14.5% multiplier effect, but overall in the third year the economy had recovered from the output losses incurred during the 1983-84 recession.

Let us now compare this performance with the current adjustment program for Portugal, as shown in the table below with quarterly values.

During the first year, the pre-Troika PEC adjustment program achieved a reduction in the current account deficit of only 2.8% at a cost of 1.4% in output. The capital effect was responsible for a decline of 3.9% in growth, but was almost offset by a trade multiplier effect of 3.0%.

For the duration of the 3-year IMF adjustment program, the current account deficit was reduced by 8.8 percentage points at a cost of 8.1% in output caused by the program’s effect on capital flows and residual price-volume effects. However, its foreign trade multiplier offset was just 4.8%, which explains why the economic recession has deepened to 5.2% (including the negative impact of terms of a terms of trade improvement brought about an appreciating Euro).

At the end of the program’s three-year period, the adjustment achieved in the current account was similar to that of the previous programs (8.8% against 7.7% and 10.1% in 1978 and 1983, respectively). Yet, this time it took twice as long and the cost in terms of output more than doubled (a 5.2% fall now, against a slowdown of 2.7% in 1978 and a loss of 2.1% in 1983).

In summary:

1) The program achieved its objectives (the current account adjustment and a return to private debt markets); but:

2) It required twice the duration and the output losses of past programs;

3) The banking sector restructuring and fiscal consolidation were negligible. Public debt increased 23.5 percentage points to reach 141.2% of GDP at the end of the program;

4) The social burden was significant, with the unemployment rate rising two percentage points to 14.4%; and

5) There was a minor (0.8%) improvement in productivity because the decline in output was close to the loss of jobs (6%).

For these reasons the Portuguese adjustment must be classified as a pyrrhic victory, which, if repeated, will ruin the country.

Saturday, 15 September 2012

Why the IMF therapy is not working in Ireland

After a remarkable economic success based on market capitalism, Ireland has drifted back into misery since the crisis of 2008 and risks turning into a Southern European type of state capitalism. Back in January 2011 we explained in this blog (see here) why the IMF program for Greece’s external adjustment would not work. Some of the reasons given then apply equally to Ireland (or Spain for that matter).

First, the Troika misdiagnosed the situation as a liquidity problem while in fact Ireland and Greece faced a solvency problem (albeit of a different nature).

Then, they treated the problem of excessive leverage in the wrong way. The two major mistakes in Ireland were the conversion of private debt into public debt and the reliance on internal devaluation to deleverage. It is easy to see why both policies were wrong.

Ireland had a typical situation faced by a family with irresponsible children that took excessive debt to pay for gambling losses at the Casino (or in its case to speculate in real estate). An obvious option to erase gambling debts was to default on the casino loans (in the case of the Irish real estate bubble the British and German banks). They could be charged with allowing bets that the gambler could not pay. One alternative would be to demand a debt restructuring involving partial debt forgiveness and a longer repayment period, so that with the help of family and friends (i. e. grants by national and EU institutions in the case of Irish borrowers) they could repay the remaining debt without damaging the credit of his family. Another alternative would be to ask the casino to accept an IOU without a redemption date (in case of the British and German banks accept money printed by the ECB).

Yet, the casino owners decided instead to force the collection of their loans from the children’s parents (i.e.Irish government). To save its reputation the family promised to honor the debts by putting them in their business balance sheet (the state budget in the case of Ireland). However, the debts were so huge that they would necessarily cripple an otherwise successful business (economy). It is easy to see why.

First, such an increase in leverage would bar the firm from market financing. Second, it would be forced to halt all modernization and maintenance investments. Finally, it would force the family to downsize by selling some of the best assets. Combining these three measures would inevitably lead to a lower competitiveness, declining productivity and a depressed local economy. As expected, in the last four years, investment in Ireland more than halved in real terms, while domestic demand declined by about one third.

However, the recourse to internal devaluation only made things worse. Imagine that the clientele of the parents business was mostly local (i.e. produced non-tradable goods in economists’ parlance). Therefore, cutting the wage of their workers would reduce its sales proportionally and reduce further the firms’ debt capacity.

Moreover, reducing nominal contracts in the labor market without a concomitant reduction in credit markets would inevitably lead to an increase in non-performing loans (which in 2011 indeed rose from 12% to 20%).

It is obvious that the policy of switching the debt burden from the private to the public sector only made things worse in Ireland. What we said about Greece applies equally to Ireland. It has only three options: a) to force a significant hair-cut on its bond-holders, b) to receive a major grant from other EU countries, or c) a mix of both. None of these is a pleasant solution but there is no other way out.

First, the Troika misdiagnosed the situation as a liquidity problem while in fact Ireland and Greece faced a solvency problem (albeit of a different nature).

Then, they treated the problem of excessive leverage in the wrong way. The two major mistakes in Ireland were the conversion of private debt into public debt and the reliance on internal devaluation to deleverage. It is easy to see why both policies were wrong.

Ireland had a typical situation faced by a family with irresponsible children that took excessive debt to pay for gambling losses at the Casino (or in its case to speculate in real estate). An obvious option to erase gambling debts was to default on the casino loans (in the case of the Irish real estate bubble the British and German banks). They could be charged with allowing bets that the gambler could not pay. One alternative would be to demand a debt restructuring involving partial debt forgiveness and a longer repayment period, so that with the help of family and friends (i. e. grants by national and EU institutions in the case of Irish borrowers) they could repay the remaining debt without damaging the credit of his family. Another alternative would be to ask the casino to accept an IOU without a redemption date (in case of the British and German banks accept money printed by the ECB).

Yet, the casino owners decided instead to force the collection of their loans from the children’s parents (i.e.Irish government). To save its reputation the family promised to honor the debts by putting them in their business balance sheet (the state budget in the case of Ireland). However, the debts were so huge that they would necessarily cripple an otherwise successful business (economy). It is easy to see why.

First, such an increase in leverage would bar the firm from market financing. Second, it would be forced to halt all modernization and maintenance investments. Finally, it would force the family to downsize by selling some of the best assets. Combining these three measures would inevitably lead to a lower competitiveness, declining productivity and a depressed local economy. As expected, in the last four years, investment in Ireland more than halved in real terms, while domestic demand declined by about one third.

However, the recourse to internal devaluation only made things worse. Imagine that the clientele of the parents business was mostly local (i.e. produced non-tradable goods in economists’ parlance). Therefore, cutting the wage of their workers would reduce its sales proportionally and reduce further the firms’ debt capacity.

Moreover, reducing nominal contracts in the labor market without a concomitant reduction in credit markets would inevitably lead to an increase in non-performing loans (which in 2011 indeed rose from 12% to 20%).

It is obvious that the policy of switching the debt burden from the private to the public sector only made things worse in Ireland. What we said about Greece applies equally to Ireland. It has only three options: a) to force a significant hair-cut on its bond-holders, b) to receive a major grant from other EU countries, or c) a mix of both. None of these is a pleasant solution but there is no other way out.

Friday, 14 September 2012

Is the IMF playing ostrich in Ireland?

Since December 2010, Ireland has diligently implemented an adjustment program agreed with the so-called Troika (IMF, ECB and EU). On its 6th review in June 2013, the IMF concluded that: “Ireland’s ownership of the program remains strong and policy implementation has continued to be steadfast despite the considerable challenges. All quantitative targets for the review were met, maintaining the strong performance in earlier reviews. Fiscal, financial, and structural reforms are advancing as envisaged”. Yet, the IMF seems intent on deliberately ignoring its failure (or lying), because it acknowledges in the same report “renewed tensions in the euro area have driven up Irish bond spreads, while growth remains weak and unemployment high”.

Indeed, in terms of both costs and results, the outcome is appalling. Let us look at the results first:

The chart above from the IMF report shows that the borrowing costs are higher than at the start of the program, remain at unsustainable levels and recently have resumed its rising trend. Likewise, the external debt shows no signs of abating, as shown in the next table:

The Irish net external debt position (excluding FDI and Reserves) deteriorated 16.8% (€30 billion) since the start of the program. Moreover, the government takeover of private debts has increased the general government debt from 25% of GDP in 2007 to 108% in 2011 and the IMF forecasts that it will increase to 121% of GDP in 2013.

Finally, let us look at the bank recapitalization. This program was pursued through a staggering increase of Tier I capital to 16%, but it did not solve the banking system solvability and profitability. The IMF table reproduced below shows that equity losses were still 20% in 2011, while the percentage of non-performing loans had increased from 12.1% to 19.5%.

So far for the results!

Unfortunately, the adjustment costs are equally dismal. The following table gives further details:

Suffice to say, Irish production (GNP) is still 11.8% less than it was four years ago and may fall again in 2012. Meanwhile, unemployment has reached 15% and might continue to rise despite a return to massive emigration. For instance, it is estimated that between 1976 and 2011, about 7.5% of native Irish in their twenties emigrated.

With such dismal results obtained at such an appalling cost, one must conclude that the IMF is playing ostrich in Ireland. Indeed, some observers may even wonder whether Ireland will become another Greece. So, it is not too soon to question whether the program is taking too long to work or it is fundamentally flawed.

Indeed, in terms of both costs and results, the outcome is appalling. Let us look at the results first:

The chart above from the IMF report shows that the borrowing costs are higher than at the start of the program, remain at unsustainable levels and recently have resumed its rising trend. Likewise, the external debt shows no signs of abating, as shown in the next table:

The Irish net external debt position (excluding FDI and Reserves) deteriorated 16.8% (€30 billion) since the start of the program. Moreover, the government takeover of private debts has increased the general government debt from 25% of GDP in 2007 to 108% in 2011 and the IMF forecasts that it will increase to 121% of GDP in 2013.

Finally, let us look at the bank recapitalization. This program was pursued through a staggering increase of Tier I capital to 16%, but it did not solve the banking system solvability and profitability. The IMF table reproduced below shows that equity losses were still 20% in 2011, while the percentage of non-performing loans had increased from 12.1% to 19.5%.

So far for the results!

Unfortunately, the adjustment costs are equally dismal. The following table gives further details:

Suffice to say, Irish production (GNP) is still 11.8% less than it was four years ago and may fall again in 2012. Meanwhile, unemployment has reached 15% and might continue to rise despite a return to massive emigration. For instance, it is estimated that between 1976 and 2011, about 7.5% of native Irish in their twenties emigrated.

With such dismal results obtained at such an appalling cost, one must conclude that the IMF is playing ostrich in Ireland. Indeed, some observers may even wonder whether Ireland will become another Greece. So, it is not too soon to question whether the program is taking too long to work or it is fundamentally flawed.

Wednesday, 12 September 2012

No país do faz de conta

Já não bastava vivermos num país onde governantes como Miguel Relvas, Sócrates e outros ex-jotas fizeram de conta que tinham tirado uma licenciatura. Também agora a Troika, para disfarçar que não sabe o que anda a fazer, faz de conta que o dito “bom aluno” passou na 5ª avaliação. Na verdade, tal como um professor ajuda os alunos fracos dando-lhes mais tempo e uns valores a mais, também a Troika teve de dar ao governo mais dois pontos percentuais e mais um ano para cumprir os objectivos para o défice.

Depois do desastre da Grécia, a Troika precisava desesperadamente de mostrar que a sua terapia baseada numa desvalorização salarial funciona numa zona monetária. Por isso, desde o início que isentou Portugal da maioria dos objectivos quantitativos tradicionais e irá continuar a fingir que o país está a cumprir as metas enquanto a situação da população e da economia se degrada cada vez mais.

Por sua vez o governo fingiu que ia resolver o problema do défice pela via da despesa e não da receita. Lembram-se dos famosos 1/3 de receita e 2/3 de cortes de despesa para reduzir o défice em 7,5 mil milhões de Euros? Pelos vistos a execução orçamental até à data mostra uma quebra acentuada nas receitas e uma redução das despesas insignificante (se excluirmos os cortes nos salários da função pública e nas reformas).

Um exemplo ilustrativo desta política do faz de conta do governo é por demais evidente nos tão falados cortes nas PPPs e nas rendas excessivas dos oligopólios concessionados.

Por exemplo, a dita renegociação das PPPs foi uma montanha que pariu um rato. Segundo a comunicação social o governo terá poupado nesta 1ª fase da renegociação perto de mil milhões de euros (isto é, 1/3 do total previsto). Desconheço se a esse montante foi deduzido o montante das indemnizações a pagar aos concessionários por quebra de contrato. De qualquer forma a poupança é fictícia pois tratou-se apenas de cancelar obras por iniciar ou em curso e da transferência de responsabilidades nas obras de manutenção. Imagine que você tinha contratado fazer um prédio de 10 andares mas como não conseguiu a totalidade do financiamento instruiu o construtor para construir apenas 5 andares. Chamaria a essa redução poupança? Claro que não! Considerava que tinha cancelado, adiado ou reduzido o seu investimento.